Economy

CBN Gives Hope to Minority Shareholders of Defunct Skye Bank

By Dipo Olowookere

The Central Bank of Nigeria (CBN) on Tuesday said efforts would be made to ensure minority shareholders of the defunct Skye Bank Plc do not completely lose their investments in the financial institution.

Governor of the CBN, Mr Godwin Emefiele, while addressing newsmen yesterday in Abuja, disclosed that the decision to revoke the operating license of the lender was done in the interest all stakeholders.

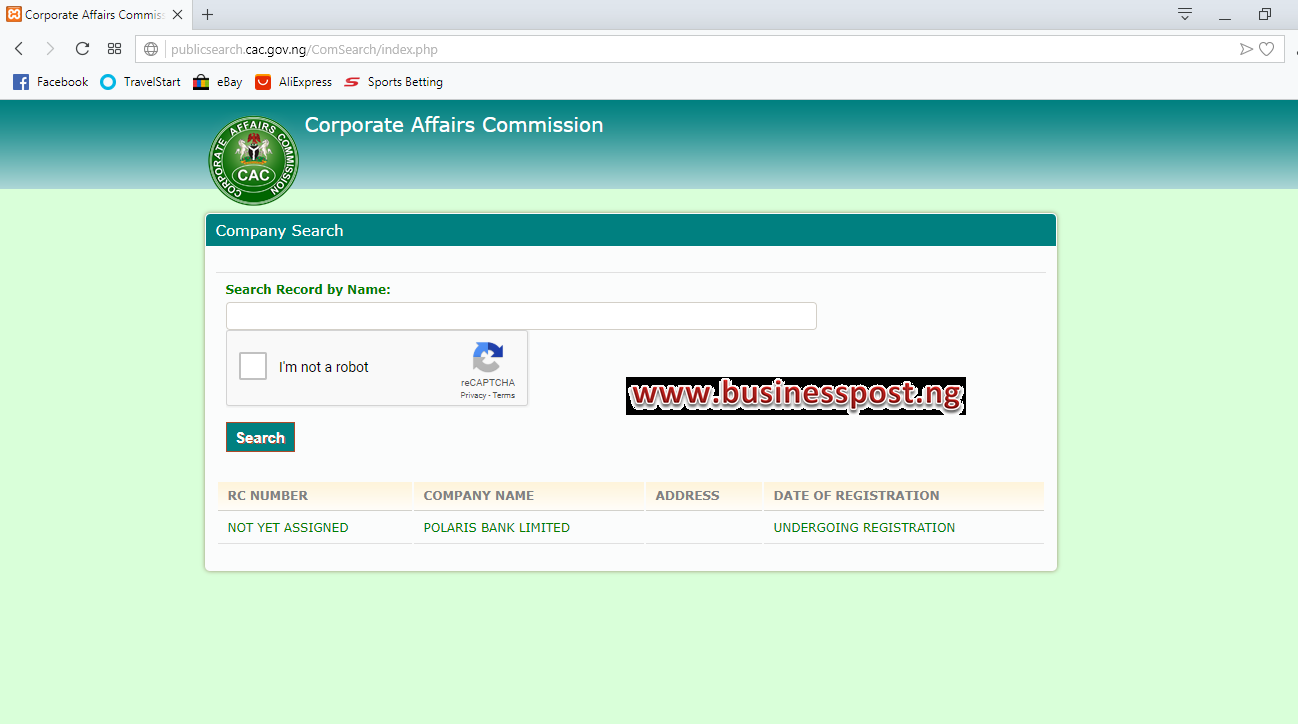

However, the central bank chief said the minority shareholders of the financial institution, which has been nationalised to Polaris Bank Limited, would have the value of their investment “substantially whittled down.”

But Mr Emefiele did not state how the apex bank plans to compensate the small investors in the lender and the process.

Last Friday night, the central bank nationalised Skye Bank and created a bridge bank called Polaris Bank Limited.

Hours later, the Nigerian Stock Exchange (NSE) announced that from Monday, September 24, 2018, trading on the shares of Skye Bank on its platform would be suspended following the regulatory action.

This left shareholders of the bank devastated, giving up any hopes of getting anything from the lender.

But taking questions from newsmen on Tuesday, Mr Emefiele said, “The situation with Skye Bank like you all know is that as at two years ago, when we took over [its affairs], the bank had slipped into negative capital as a result of non-performing loans (NPLs).

“At that time, we compelled the entire board and the executive management to resign and they willingly left.”

“Before we conducted a forensic audit [on its books], the hole was about N370 billion and after the audit, it came to the level that it is right now, close to about N800 billion and what we decided to do is that, having established the problem, and with the decision to invest taxpayers money in this company, though as a loan, then there was a need to let shareholders know, particularly, I repeat, particularly, those we consider to be prominent and important shareholders that they’ve lost their investments.

“We will try just like we have done in the situation of depositors to make sure that the small investors (minority shareholders) remain protected under some arrangement, but notwithstanding that the fact that their holdings would be substantially whittled down,” Mr Emefiele said at the briefing monitored by Business Post in Lagos yesterday.

The CBN chief explained that in order to avoid future legal issues, the name of the bank had to be changed from Skye Bank to Polaris Bank.

“The name has to be changed for legal reasons, having gotten to a point where the CBN and government have invested about N800 billion in this bank, at some points, it must be seen to be owned by the CBN until we find investor that can pay a fair value for this enterprise. That is the compelling reason the name had to change,” he said.

Business Post reports that as at the last day shares of Skye Bank were traded on the NSE, last Friday, they went for 77 kobo per share.

By Aduragbemi Omiyale

A strategic non-equity capital of N2 billion has been pumped into one of Nigeria’s emerging integrated agribusiness companies, Zichis Agro Allied Industries Plc.

Chilla Entertainment is one of the promoters of Zichis. The capital injection reaffirms the investor’s confidence in the company’s vision, growth prospects, and long-term value creation strategy.

In a note to the Nigerian Exchange (NGX) Limited, the funds will be a long-term liability in the company’s balance sheet to be redeemed at a future date in terms of debt conversion to equity during a public offer or rights issues.

It is designed to transform Zichis into one of Nigeria’s leading agro-industrial enterprises with a fully integrated value chain spanning feed production, poultry farming, palm cultivation, and agro-processing.

The newly injected capital will primarily be deployed towards expanding the firm’s operational capacity and strengthening its working capital position.

Key areas of investment include a significant increase in poultry production capacity, strengthening of the company’s integrated livestock value chain, and enhancement of operational efficiency and output levels.

In addition, the N2 billion would be used to increase the procurement of raw materials to support higher production volumes, grow the supply chain for the organisation’s feed mill operations, and position the business to meet growing demand within Nigeria’s livestock and poultry sectors.

Also, Zichis will accelerate the cultivation of its newly acquired 2,000-acre agricultural land in Ogun State to significantly increase its agricultural asset base and future revenue-generating capacity.

Zichis is strategically positioning itself to capitalise on these opportunities through its diversified agribusiness model, expanding production footprint, and disciplined execution strategy.

The endgame is to enhance shareholder value, expand operational capacity, build sustainable competitive advantages, and deliver long-term returns to investors.

Recently, the board and management visited the Nigerian Institute for Oil Palm Research (NIFOR) in Edo State for a strategic partnership on the acquisition of high-yield oil palm seedlings and the implementation of modern cultivation techniques across its expanding palm estate.

This collaboration is expected to enhance productivity, improve long-term yields, and support the company’s objective of becoming a major participant in Nigeria’s growing palm oil value chain.

Zichis reaffirmed its commitment to maintaining the highest standards of corporate governance, transparency, accountability, and regulatory compliance.

By Adedapo Adesanya

The Manufacturers Association of Nigeria (MAN) has called for stakeholder engagement over the Senate’s request for a ban on the import of textile materials.

The Director-General of the association, Mr Segun Ajayi-Kadir, said such a policy without proper engagement will only lead to failure.

“I want to appeal to the National Assembly: let us not go down this route the same way again. The failure of policy in Nigeria has principally been due to a lack of stakeholder engagement. You cannot shave a man’s head in his absence,” he said on Channels TV breakfast show on Wednesday.

“We pass resolutions, introduce policies, and enact laws that do not substantially reflect what is happening on the ground. That is why well-intentioned moves fail to achieve their objectives.

“We need stakeholder engagement. We need to bring all the existing textile industries to the table and ask them, ‘When, how, and where can you scale?’ We have an idea of the national demand, and we know the reasons why they are operating below 30 per cent of installed capacity. The question is, does the government have the political will to do what it takes to help them deliver?”

On Tuesday, the Senate asked the federal government to ban the importation of textile materials in a bid to boost local production and revive the country’s struggling textile industry.

It urged the federal government, through the Ministries of Agriculture and Trade and Investment, to take urgent steps to resuscitate textile manufacturing across the country, particularly along the Kaduna-Kano industrial corridor, citing its potential to create jobs and address rising youth unemployment and insecurity.

Mr Ajayi-Kadir said the country can meet its textile needs, but believes revival of the industry has to go beyond “passing” resolutions.

“It needs to be actively supported by measures that we have consistently recommended but have not yet been implemented,” the MAN chief said.

“For instance, are we going to enforce the patronage of made-in-Nigeria textiles within the government? When the National Assembly passed this resolution, how many of them were wearing made-in-Nigeria garments? If you look closer, how many of us are driving cars assembled in Nigeria?

“If you legislate a ban on textile imports, it must go hand-in-hand with the diligent implementation of Executive Order 003 and a ‘Nigeria First’ mindset. Are we going to enforce it from the Presidency to the National Assembly, the military, uniformed agencies, and even schools? Are we ready to enforce a ‘Nigeria Day’ where everyone is obliged to wear what is made in Nigeria?

“Is the government going to do its bit? Are we going to reject textile, garment, or uniform items in the budget unless they show a direct connection to local production? Are we going to muster what it takes to effectively implement the 30 per cent Common External Tariff (CET) on imports from third countries? Are we going to secure our borders so that the ban does not come to nought?

“A major conversation needs to take place for us to be serious about enforcing an import ban. It is not just by fiat,” he said on the show.

By Adedapo Adesanya

The Minister of Finance, Mr Taiwo Oyedele, has endorsed the 2026 Article IV Mission Concluding Statement on Nigeria by the International Monetary Fund (IMF), saying the report provides further independent validation that the bold and necessary reforms undertaken under the leadership of President Bola Tinubu are strengthening macroeconomic stability.

He noted the IMF’s overall positive assessment of the country’s economic reform programme, which projected economic growth of 4.1 per cent in 2026 despite persistent poverty, food insecurity, and renewed inflationary pressures arising from rising global fuel and food prices.

The Fund said that although the reforms have delivered improved macroeconomic outcomes, conditions remain difficult for many Nigerians. According to the IMF, poverty reached 63 per cent based on the national poverty line, while an estimated 27 million Nigerians faced food insecurity in late 2025.

According to Mr Oyedele, the IMF observed that reforms implemented over the past three years have yielded improved macroeconomic outcomes and enhanced Nigeria’s resilience to external shocks.

He said the Fund specifically highlighted improvements in foreign exchange market functioning, stronger external buffers, ongoing fiscal and revenue reforms, banking sector resilience, and growing macroeconomic stability.

“These developments affirm that Nigeria is moving in the right direction and is better positioned to withstand global economic uncertainties than at any time in recent years.

“The government is particularly encouraged by the IMF’s recognition that the difficult but necessary decisions to end fuel subsidies, eliminate deficit monetisation, liberalise the foreign exchange market, and strengthen fiscal discipline have contributed significantly to reducing vulnerabilities and rebuilding confidence in the economy. The report notes that Nigeria now faces global shocks with stronger policy frameworks and buffers than before.”

Mr Oyedele said the recent conflict in the Middle East has created new challenges for economies around the world through higher energy prices, rising food costs, tighter financial conditions, and disruptions to global supply chains. While these developments present inflationary pressures, the IMF acknowledged that Nigeria has demonstrated notable resilience.

He added that despite significant increases in global energy prices, the foreign exchange parallel market premium has remained below five per cent, sovereign spreads have remained broadly stable, and investor confidence has been preserved.

“The IMF further noted that Nigeria is well-positioned to benefit from higher energy prices through stronger export earnings, improved fiscal revenues, and increased foreign exchange inflows.”

The minister explained that the federal government remains focused on translating these opportunities into long-term gains by increasing crude oil production, expanding domestic refining capacity, growing gas production and exports, and attracting new investments across the energy value chain.

“While challenges remain, the direction is clear, and the foundations are stronger. The ultimate objective of these reforms is not merely improved economic indicators, but better outcomes for all Nigerians: lower inflation, decent jobs, higher incomes, greater economic opportunity, and a better quality of life,” he said.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn