Economy

TSA: Court Orders Skye Bank, UBA, 5 Others to Remit $793m to FG

By Modupe Gbadeyanka

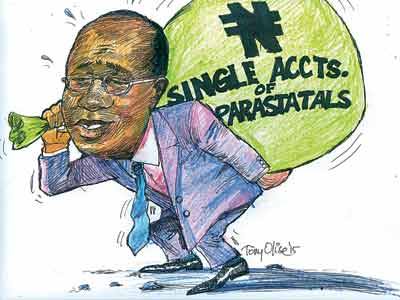

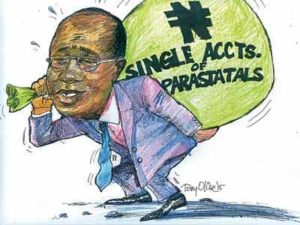

Seven banks operating in Nigeria have been directed by a Federal High Court sitting in Lagos to remit about $793.2 million allegedly hidden by them in violation of the Federal Government’s Treasury Single Account (TSA) policy.

The affected lenders include Skye Bank, United Bank for Africa (UBA), Diamond Bank, First Bank Nigeria Limited, Fidelity Bank, Keystone Bank Limited, and Sterling Bank.

In his ruling yesterday, Justice Chuka Obiozor ordered the banks to remit the various amounts into the designated Federal Government’s Asset Recovery dollars account domiciled with the Central Bank of Nigeria (CBN).

According to court documents filed by counsel to the Attorney General of the Federation (AGF), Mr Yemi Akinseye-George, “a total of $367.4 million was illegally hidden by three government agencies in UBA, while a sum of $41 million was illegally kept in a NAPIMS fixed deposit account with Skye Bank.”

The documents indicated that “$277.9 million was hidden in Diamond Bank; $18.9 million in First Bank; $24.5 million in Fidelity Bank; $17 million in Keystone Bank; and $46.5 million in Sterling Bank.”

A lawyer from Mr Akinseye-George’s law firm, Mr Vincent Adodo, who deposed to a 15-paragraph affidavit in support of an ex parte application filed by the AGF, stated that “seven banks colluded with federal government officials to hide the funds in breach of the government’s TSA policy.”

“The funds were revenues, donations, transfers, refunds, grants, taxes, fees, dues, tariffs etc accruable to the Federal Government from different ministries, departments, parastatals and agencies,” said Mr Adodo.

Mr Adodo said the banks had failed to remit the funds to the TSA domiciled in the CBN in violation of the guidelines issued by the Accountant General of the Federation which fixed September 15, 2015 as the deadline for such funds to be moved.

The 1st to 7th respondents (banks), he said, “in collaboration with and/or collusion with unknown officials of the Federal Government, conspired to disobey the relevant constitutional provisions, thereby depriving the Government of the Federal Republic of Nigeria of funds belonging to it, which are needed urgently to fund pressing national projects under the 2017 budget.”

Among the allegedly culpable government agencies is the National Petroleum Development Company.

Moving the ex-parte application on Thursday, Mr George said “it would best serve the interest of justice for Justice Obiozor to order the banks to remit the funds to the Federal Government, to prevent the funds from being moved or dissipated.

“The withheld funds are urgently required for the implementation of the 2017 budget. The budget has a lifespan of 12 months and we are already in the middle of the year. By hiding these funds, the Federal Government is being forced to borrow money from these commercial banks at exorbitant interest rate,” Mr Akinseye-George added.

After listening to the counsel, Justice Obiozor granted the interim orders.

He directed that the order should be published in a national daily newspaper.

He, subsequently, adjourned till August 8, 2017, for anyone interested in the funds to appear before him to show cause why the interim orders should not be made permanent.

‘We are not guilty’

In a swift response to the judge’s decision, Fidelity Bank Plc denied holding any wrongdoing.

Mr Charles Aigbe, the Divisional Head, Brand and Communications at the bank, said since the commencement of the TSA policy, all TSA related accounts held by the bank were fully disclosed to the authorities.

“We do not have any TSA related account with a balance of $24.5m in Fidelity Bank which has not been remitted to the authorities,” Mr Aigbe said in a statement.

“This matter is coming to us as a surprise. We are therefore reaching out to the Office of the Attorney-General of the Federation to ascertain which account or parastatal they are referring to with a view to carrying out a detailed reconciliation,” he added.

Also, UBA’s Group Head, Marketing & Corporate Communications, Bola Atta, in a statement on Friday afternoon, said her bank “has fully remitted all NNPC/NLNG dollar deposits since August 24, 2016.”

“We hereby emphasise that none of such funds are currently in the Bank’s books. Our action was further corroborated by a clearance memo published by CBN on its website on same date (http://www.cbn.gov.ng/Out/2016/CCD/UBAPress%20Statement240816.pdf).

“We would like to thank all our customers, business partners and other stakeholders who have reached out to us on account of this judgement,” she said.

Additional information from Premium Times

By Adedapo Adesanya

Workers at Seplat Energy will resume work after a strike action that impacted production was called off by the Petroleum and Natural Gas Senior Staff Association of Nigeria (PENGASSAN) over the weekend, with the company issuing written commitments on pay rises.

Top employees began an indefinite strike last Friday as talks over a collective bargaining agreement and staff welfare issues broke down. The action came at a time when Nigeria is seeking to maximise production amid rising global oil prices.

According to Reuters, in an April 4 letter to the chief executive of Seplat Nigeria, Mr Roger Brown, PENGASSAN said it had directed members at the local energy firm to immediately suspend industrial action after negotiations resumed with the Nigerian National Petroleum Company (NNPC) Limited. Other less-skilled workers are covered by the Nigeria Labour Congress (NLC) and did not partake in the strike with PENGASSAN.

The union said talks on a 2026 collective bargaining agreement would continue, with the aim of concluding outstanding issues by April 13. However, according to the publication, the union did not disclose more details about its financial demands.

“We can confirm that the union has suspended its notice of industrial action to allow negotiations to conclude on outstanding items within an agreed framework,” Seplat spokesperson, Mr Ogechukwu Udeagha, said, adding that “operations are recommencing at our various locations.”

Seplat Energy’s group production averaged 131,506 barrels of oil equivalent per day in 2025, according to its latest audited results. That is the equivalent of around 7 per cent–9 per cent of Nigeria’s total liquids production.

The company expects output to rise to 155,000 barrels of oil equivalent per day, making any sustained disruption particularly sensitive for Nigeria’s supply outlook. This comes as it seeks to scale production while remaining a major supplier of gas to Nigeria’s domestic power market.

With the company’s output expected to rise, any prolonged disruption would have significantly impacted Nigeria’s oil supply and fiscal outlook.

By Dipo Olowookere

The weekly turnover of the Nigerian Exchange (NGX) Limited shrank by 27.70 per cent or 1.094 billion equities, partly due to the inability of market participants to trade last Friday as a result of the Good Friday public holiday declared by the federal government.

In the week, investors bought and sold 2.856 billion equities worth N113.597 billion in 215,287 deals versus the 3.950 billion equities valued at N201.312 billion transacted in 359,642 deals in the preceding week.

The activity chart was led by the financial services industry with 1.811 billion shares valued at N61.901 billion in 86,818 deals, contributing 63.41 per cent and 54.49 per cent to the total trading volume and value, respectively.

The services sector traded 299.895 million stocks worth N2.966 billion in 13,797 deals, and the ICT segment exchanged 183.233 million equities for N14.654 billion in 25,287 deals.

Wema Bank, Access Holdings, and Secure Electronic Technology accounted for 734.659 million shares worth N14.134 billion in 12,319 deals, contributing 25.72 per cent and 12.44 per cent to the total trading volume and value apiece.

Data from the NGX said 29 stocks gained weight versus 47 stocks of the previous week, as 57 shares lost weight versus 45 shares in the preceding week, while 62 equities closed flat versus 56 equities a week earlier.

Multiverse led the gainers’ chart after it gained 20.66 per cent to trade at N20.15, UPDC REIT appreciated by 15.49 per cent to N8.20, International Energy Insurance chalked up 12.54 per cent to quote at N3.32, Austin Laz grew by 10.47 per cent to N4.43, and Unilever Nigeria rose by 10.00 per cent to N103.40.

Conversely, Secure Electronic Technology topped the losers’ table after it lost 21.54 per cent to close at N1.02, John Holt declined by 18.47 per cent to N15.45, May and Baker depreciated by 16.57 per cent to N35.00, Aluminium Extrusion moderated by 16.27 per cent to N10.55, and Legend Internet slipped by 16.00 per cent to N6.30.

Business Post reports that the All-Share Index (ASI) was up by 0.39 per cent to 201,698,89 points, and the market capitalisation rose by 0.65 per cent to N129.806 trillion.

In the same vein, all other indices finished higher apart from the main board, insurance, MERI Value, consumer goods, industrial goods and growth indices, which went down by 0.29 per cent, 4.25 per cent, 0.36 per cent, 1.74 per cent, 0.24 per cent, and 0.06 per cent, respectively, while the sovereign bond index closed flat.

By Adedapo Adesanya

The NASD Over-the-Counter (OTC) Securities Exchange recorded a 3.8 per cent week-on-week decline in the 14th trading week of 2026, which had only four trading sessions.

This happened because of the public holiday observed on Friday for Easter celebrations in Nigeria and across the globe.

Last week, the market capitalisation of the bourse went down by N95.36 billion to N2.417 trillion from N2.512 trillion in Week 13, while the NASD Unlisted Securities Index (NSI) shrank by 159.39 points to 4,040.30 points from 4,199.69 points in the previous week.

In the week, there were five price losers and eight price losers led by 11 Plc, which crumbled by N94.57 to N256.60 per unit from N351.17 per unit.

MRS Oil Plc lost N39.00 to close at N171.00 per share from N210.00 per share, FrieslandCampina Wamco Nigeria Plc depreciated by N17 to N93.00 per unit from N110.00 per unit, and Central Securities Clearing System (CSCS) Plc shed N2.10 to close at N78.00 per share versus N80.10 per share.

Further, NASD Plc dropped N4.14 to end at N37.36 per unit versus N41.50 per unit, UBN Property Plc crashed by 22 Kobo to N1.98 per share from N2.20 per share, Food Concepts Plc slid by 13 Kobo to N2.87 per unit from N3.00 per unit, and Capital Bancorp Plc contracted by 10 Kobo to N1.90 per share from N2.00 per share.

On the flip side, IPWA Plc gained 55 Kobo to sell at N6.06 per unit versus N5.51 per unit, Geo-Fluids Plc appreciated by 7 Kobo to N3.25 per share from N3.18 per share, Industrial and General Insurance (IGI) Plc improved by 5 Kobo to 57 Kobo per unit from 52 Kobo per unit, Great Nigeria Insurance (GNI) Plc grew by 2 Kobo to 52 Kobo per share from 50 Kobo per share, and Acorn Petroleum Plc moved up by 1 Kobo to N1.34 per unit from N1.33 per unit.

The volume of transactions witnessed a 5,490.9 per cent surge last week to 3.5 billion units from 62.7 million units, and the value of transactions soared by 437.7 per cent to N9.7 billion from N1.7 billion. These trades were completed in 163 deals and involved 20 stocks.

The most traded stock by value was GNI Plc with N8.4 billion, followed by Okitipupa Plc with N630.5 million, Geo-Fluids Plc with N162.7 million, CSCS Plc with N57.5 million, and Friesland Campina Wamco Nigeria Plc with N37.1 million.

The most trased stock by volume was also GNI Plc with 3.4 billion units, Geo-Fluids Plc traded 50.1 million units, Okitipupa Plc transacted 21.0 million units, UBN Property Plc quoted 2.5 million units, and CSCS Plc sold 0.73 million units.

-

Feature/OPED6 years ago

Feature/OPED6 years agoDavos was Different this year

-

Travel/Tourism10 years ago

Lagos Seals Western Lodge Hotel In Ikorodu

-

Showbiz3 years ago

Showbiz3 years agoEstranged Lover Releases Videos of Empress Njamah Bathing

-

Banking8 years ago

Banking8 years agoSort Codes of GTBank Branches in Nigeria

-

Economy3 years ago

Economy3 years agoSubsidy Removal: CNG at N130 Per Litre Cheaper Than Petrol—IPMAN

-

Banking3 years ago

Banking3 years agoSort Codes of UBA Branches in Nigeria

-

Banking3 years ago

Banking3 years agoFirst Bank Announces Planned Downtime

-

Sports3 years ago

Sports3 years agoHighest Paid Nigerian Footballer – How Much Do Nigerian Footballers Earn