Economy

Nigeria: Moody’s Predicts 2.5% GDP Growth in 2017, 4% in 2018

**Affirms Country’s B1 Rating With Stable Outlook

By Modupe Gbadeyanka

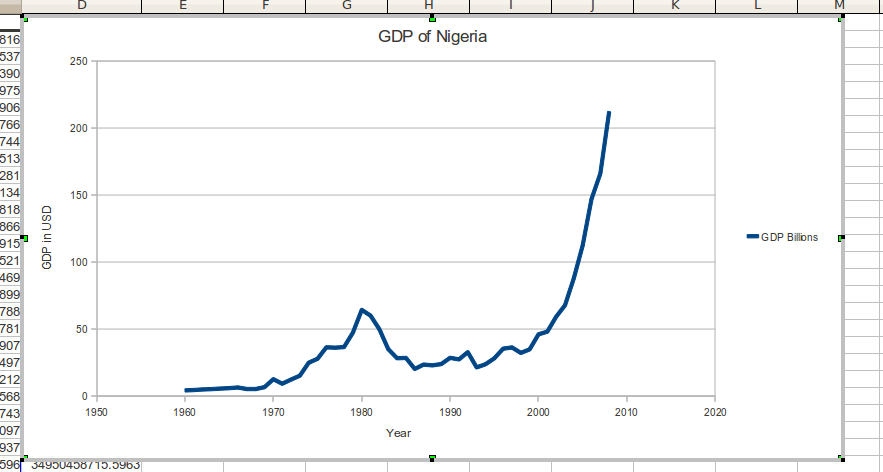

Moody’s Investors Service on Friday affirmed the B1 long-term issuer rating of the government of Nigeria with a stable outlook just as it forecasts that real GDP growth will rise to 2.5 percent in 2017 and accelerate further in 2018 to 4 percent.

The global rating firm disclosed that the key drivers for these were the medium term growth prospects remain robust despite the current challenging environment, with the rebound in oil production helping to rebalance the economy over the next two years; and the government’s balance sheet, which it said remains strong relative to its peers, resilient to the contractionary environment and temporarily elevated interest payments while the authorities pursue their efforts to grow non-oil taxes.

The long-term local-currency bond and deposit ceilings remain unchanged at Ba1. The long-term foreign-currency bond and deposit ceilings remain unchanged at Ba3 and B2, respectively.

Moody’s said it expects Nigeria’s medium term growth to remain robust, driven by the recovery in oil output and also over the near term, it expects Nigeria’s economic growth and US dollar earnings to improve in 2017, supported by a recovery in oil production.

According to Moody’s, after an estimated -1.5 percent real GDP growth in 2016, it forecasts real GDP growth to rise to 2.5% in 2017 and accelerate further in 2018 to 4%. A rebound in oil production to two million barrels per day (mbpd) will, if sustained, enhance economic growth and support the US dollar supply in the economy.

It noted that Nigeria has made significant gains in terms of governance and transparency in the oil sector. Improved availability of data, progress in restructuring the Nigerian National Petroleum Company (NNPC), rising effectiveness of operations at the refineries and a readiness to tackle difficult issues with partners (such as funding issues at the Joint Ventures) speak to a material improvement in the operating environment. The Petroleum Investment Bill (PIB bill), which had been blocked for 8 years in parliament, has been reactivated with a portion of the law drafted and passed by the Senate. Moreover, militant activity in the Niger Delta is set to wane following the resumption of payments from the government, though it will remain a threat to the recovery of the economy.

Moody’s further said the economy is also likely to benefit from the more timely implementation of the 2017 budget than its predecessor and in particular from the increase in capital spending on infrastructure which that will allow.

It also said the scarcity of Dollars, worsened by the soft capital controls imposed by the Central Bank of Nigeria (CBN), is likely to continue to negatively affect important sectors of the economy especially in services and manufacturing sectors.

“We do not expect the current policy mix to significantly change over the short term but a gradual easing of restrictions is possible as foreign currency receipts improve with rising oil production,” the firm said on Friday in a statement obtained by Business Post.

In 2017 and 2018, we expect Nigeria’s balance of payments to move back into surplus, supported by government external borrowings and a falling current account deficit. The latter is quickly reducing, supported by falling imports and increased oil production.

Depreciation of the naira, soft capital controls and current dollar scarcity have been relatively effective at constraining imports. We expect foreign exchange reserves to grow modestly in 2017. While improved foreign investor sentiment should support the rebalancing of the economy over the medium term, with the return of portfolio investors improving dollar liquidity in the country, the continued existence of a parallel, unofficial foreign exchange market is likely to act as a strong deterrent over the near term.

RESILIENT GOVERNMENT BALANCE SHEET STRONGER THAN PEERS’ DESPITE TURBULENCE

Moody’s says it expects the medium-term impact of the oil price shock on Nigeria’s government balance sheet to be contained, and recent erosion of debt affordability to be reversed.

The effect of the recent downturn on the government’s budget sheet has been contained as the authorities have been able to offset the shortfall in revenue with large cuts in capital expenditure. As a result, Moody’s forecasts a budget deficit of 3 percent of GDP in 2016, comprised of a 2 percent of GDP federal government budget deficit and around 1% of arrears split between federal, state and municipality levels of government, it explained.

Moody’s forecasts the federal government deficit to remain around 2% of GDP in 2017 and 2018, with large capital expenditure outlays resuming as the government’s cash flow situation improves. Based on these underlying projections, Nigeria’s balance sheet will continue to compare favourably with peers’, with government debt remaining well below 20% of GDP over the coming years against 55% median for B1-rated peers.

By end-2016, Moody’s estimates the government debt stock will be comprised of 85% domestic borrowing and 15% external debt, resulting in a manageable external debt profile. Government external debt amounts to just 2.9% of GDP, with interest payments set to remain low, at around $330 million dollars per annum. Domestic debt has increased significantly in recent years, reaching its current level of NGN10 trillion. Around 30% of this debt is comprised of costly T-bills, which have increased refinancing risk and interest rate exposure. However, Moody’s expects the ratio of interest payments to government revenues to peak at 20% for general government, and close to 40% of revenues for federal government in 2017.

Although debt service costs are high, Nigeria’s domestic capital market is sufficiently developed to accommodate the yearly public sector borrowing requirements of around NGN5.5 trillion. This is another positive credit feature that distinguishes Nigeria from many similarly rated peers. The country’s banking sector is well-capitalised and liquid and the national pension fund still has additional capacity. Should banking sector liquidity decline, the Central Bank of Nigeria has tools at its disposal to support appetite for government securities, including lowering the cash reserve requirement ratio from its presently high level of 22.5%. However, appetite for government securities remains strong, with all instruments remain oversubscribed.

Moody’s expects the recent increase in debt service costs to prove temporary, as a result of i) the government’ initiatives to expand the non-oil revenue base, and ii) efforts to improve the structure of government debt.

Measures by the Federal Revenue Inland Service are expected to increase non-oil revenue to around NGN4 trillion in 2016 from NGN2.5 trillion in 2015. These include a tax amnesty on penalties and interest on tax liabilities due in 2013, 2014 and 2015. However, not all the initiatives have proven successful: the independent re-appropriation of revenues from the ministries departments and agencies (MDAs) has yielded disappointing results so far. Such outcomes highlight the considerable execution risks inherent in the transition to a less oil-dependent federal budget, and the implications for the government balance sheet should it not meet its objectives.

The government’s medium-term debt strategy should also help to lower the interest burden. The debt strategy is geared towards exchanging costly short-term debt with long-term concessional borrowing. Although a portion of future external borrowings are expected to be raised through the Eurobond markets, this is likely to be complemented with ongoing support from other multilateral institutions including the African Development Bank and the World Bank. The combined effect of these measures should help to bring interest payments/general government revenues down to 16.8% by 2018, from an estimated 19.8% in 2016.

RATIONALE FOR THE OUTLOOK AT STABLE

The stable outlook is driven by Moody’s view that the downside risks posed by the weakening of the country’s fiscal strength, and the external and economic pressures anticipated this year and next, are balanced by Nigeria’s strengths, which exceed those of sovereigns rated below B1. In 2016, Nigeria’s external vulnerability indicator of 31% will remain far below the expected B1 median of 51%, while its debt-to-GDP of 16.6% will remain far below the expected B1 median of 55%. Set against that, its expected debt servicing burden in terms of interest payments to revenue of 19% is more than double the B1 median of 9%. To a large extent, Moody’s believes that this reflects Nigeria’s underdeveloped public sector revenue base, a credit weakness that the administration is attempting to address.

WHAT COULD CHANGE THE RATING UP

Positive pressure on Nigeria’s issuer rating will be exerted upon: 1) successful implementation of structural reforms by the Buhari administration, in particular with respect to public resource management and the broadening of the revenue base; 2) strong improvement in institutional strength with respect to corruption, government effectiveness, and the rule of law; 3) the rebuilding of large financial buffers sufficient to shelter the economy against a prolonged period of oil price and production volatility.

WHAT COULD CHANGE THE RATING DOWN

Nigeria’s B1 issuer rating could be downgraded in the event of 1) a greater-than-anticipated deterioration in the government’s balance sheet or continued erosion of debt affordability, for example resulting from the failure to implement revenue reform; and 2) lower than expected medium term growth, for example as a result of delays in implementing key structural reforms, especially in the oil sector, or continued militancy in the Niger Delta, which undermine the level of oil production over the medium-term.

GDP per capita (PPP basis, US$): 6,184 (2015 Actual) (also known as Per Capita Income)

Real GDP growth (% change): -1.5% (2016 Estimate) (also known as GDP Growth)

Inflation Rate (CPI, % change Dec/Dec): 19% (2016 Estimate)

Gen. Gov. Financial Balance/GDP: -2.9% (2016 Estimate) (also known as Fiscal Balance)

Current Account Balance/GDP: -0.6% (2016 Estimate) (also known as External Balance)

External debt/GDP: 4.2% (2016 Estimate)

Level of economic development: Low level of economic resilience

Default history: No default events (on bonds or loans) have been recorded since 1983.

On 7 December 2016, a rating committee was called to discuss the ratings of the Government of Nigeria. The main points raised during the discussion were: The issuer’s economic fundamentals, including its economic strength, have not materially changed. The issuer’s fiscal or financial strength, including its debt profile, has not materially changed. The issuer’s susceptibility to event risks has not materially changed. Other views raised included: the issuer’s institutional strength/framework, have not materially changed. The issuer’s governance and/or management, have not materially changed.

The principal methodology used in these ratings was Sovereign Bond Ratings published in December 2015. Please see the Rating Methodologies page on www.moodys.com for a copy of this methodology.

The weighting of all rating factors is described in the methodology used in this credit rating action, if applicable.

By Adedapo Adesanya

The Nigeria Customs Service (NCS) is seeking a reduction in import duty exemptions, which rose to N34 trillion, limiting its ability to increase its revenue generation threshold.

The Comptroller-General of the Customs Service, Mr Adewale Adeniyi, disclosed that the value of import duty exemption certificate approvals increased to that level in 2025, describing the policy as one of the major factors restricting its revenue generation.

At an investigative session of the Senate Committee on Finance with revenue-generating agencies in Abuja on Monday, Mr Adeniyi explained that government fiscal policies have continued to impact the revenue-generating capacity of the Customs Service, both positively and negatively.

“The NCS would have generated significantly higher revenue over the years if not for government-approved import duty waivers and other external factors affecting collections,” he said.

He added that the Import Duty Exemption Certificate scheme, introduced in March 2020, accounted for about N34 trillion in approvals in 2025, with nearly 60 per cent covering duty-free importation of military hardware due to Nigeria’s prevailing security challenges.

Other government-backed duty waivers, he noted, covered the importation of Compressed Natural Gas (CNG), electric and hybrid vehicles, healthcare equipment and medical supplies, industrial machinery and manufacturing inputs, as well as food import intervention programmes.

While acknowledging the impact of the waivers on Customs revenue, Mr Adeniyi argued that fiscal policy should not be assessed solely on the basis of revenue generation but also on its broader economic and social objectives.

He, however, urged the federal government to establish stronger monitoring mechanisms to ensure beneficiaries of duty waivers deliver the intended economic outcomes, including lower consumer prices, increased local production and improved healthcare access.

The committee also expressed displeasure over the absence of several heads of government agencies invited to the hearing, including the Nigerian Civil Aviation Authority (NCAA), Small and Medium Enterprises Development Agency of Nigeria (SMEDAN), Industrial Training Fund (ITF), and the Federal Medical Centre (FMC), Jabi.

The Chairman of the Senate Committee on Finance, Mr Sani Musa, warned that the affected chief executives must appear at the committee’s next sitting or face severe sanctions under the Senate’s rules.

In the competitive world of online trading, finding a trading brokerage partner that balances reliability, technological innovation, and accessible conditions is essential. Headway broker has emerged as a significant player, currently serving over 4 million users globally.

In this article, we take a detailed look at what makes this broker for trading a notable option for both novice and experienced traders.

Headway Regulatory Foundation and Safety

Safety is the cornerstone of any trading relationship. Headway broker operates under the regulation and licensing of the Financial Sector Conduct Authority (FSCA). This regulatory oversight ensures that the broker adheres to strictly defined standards for transparency and operational conduct, providing traders with an added layer of security and confidence when managing their portfolios.

Trading Platforms and Instruments

Efficiency in trading Forex and other markets is driven by the tools at your disposal. Headway provides a robust technological trading ecosystem:

Industry-Standard Platforms: The broker fully supports MetaTrader 4 (MT4) and MetaTrader 5 (MT5), the most widely used platforms for technical analysis and automated trading.

Proprietary Mobile App: For traders who prioritize mobility, Headway offers its own custom-built trading app. It is readily available for download on both Google Play and the App Store, allowing for seamless account management and trading on the go.

Diverse Market Access: Traders have a wide range of opportunities with access to over 300 trading instruments, ensuring plenty of choice for different strategies and asset classes.

Trading Account Types Offered by Headway

Headway broker understands that every trader enters the market with a different level of experience:

Three Account Tiers: To ensure inclusivity, the broker offers three distinct types of accounts (Cent, Standard and Pro), tailored to suit different levels of expertise and capital requirements.

Demo Account: For those looking to refine their skills without financial risk, Headway provides a comprehensive demo trading account. This is the perfect environment to practice strategies, understand how the platform works, and gain confidence before transitioning to live trading.

Customer Support and Incentives

Headway supports its user base with comprehensive resources and financial incentives:

24/7 Technical Support: Market fluctuations happen at any time. Headway provides round-the-clock technical support for the traders, ensuring that help is always available whenever a question or issue arises.

150$ No Deposit Bonus: To help new traders get started, Headway offers a $150 no deposit bonus. This is an excellent way to test the broker’s execution speed and trading environment with zero initial risk.

IB Partnership Program: Beyond individual trading, Headway fosters growth through its Introducing Broker (IB) partnership program. This allows partners to build their business and earn commissions by referring new traders to the platform.

Conclusion

With its combination of FSCA regulation, a vast range of instruments, and modern platforms like MT4, MT5, and its own proprietary app, Headway FX broker provides a comprehensive environment for modern traders. Whether you are using the demo account to hone your skills or taking advantage of the 150 no deposit welcome bonus, this broker offers the stability and tools needed for your trading journey.

By Adedapo Adesanya

The NASD Over-the-Counter (OTC) Securities Exchange rose by 0.40 per cent on Monday, July 13, buoyed by buying interest in 11 Plc, Central Securities Clearing System (CSCS) Plc and UBN Property Plc, which offset the profit-taking in Food Concepts Plc, the parent company of Chicken Republic.

11 Plc gained N20.69 to end at N227.64 per share compared with last Friday’s price of N206.95 per share, CSCS Plc grew by N1.83 to N91.48 per unit from N89.65 per unit, and UBN Property Plc added 1 Kobo to sell at N1.81 per share versus N1.80 per share.

On the flip side, Food Concepts Plc depreciated by 24 Kobo to close at N2.45 per unit, in contrast to the preceding session’s N2.69 per unit.

As a result, the market capitalisation increased by N9.2 billion to N2.587 trillion from N2.578 trillion, and the NASD Security Index (NSI) improved by 15.33 points to 4,311.67 points from 4,296.34 points.

Yesterday, the volume of securities traded by investors surged by 615.9 per cent to 9.1 million units from the previous 1.3 million units, and the value of securities rose by 997.1 per cent to N320.4 million from the preceding session’s N29.2 million, while the number of deals decreased by 12.5 per cent to 28 deals from last Friday’s 32 deals.

At the close of trades, Great Nigeria Insurance (GNI) Plc remained the most active stock by value on a year-to-date basis, with 3.4 billion units valued at N8.4 billion, followed by Infrastructure Credit Guarantee (Infracredit) Plc with 2.3 billion units worth N6.5 billion, and CSCS Plc with 73.9 million units exchanged for N5.2 billion.

GNI Plc also closed the session as the most traded stock by volume on a year-to-date basis, with 3.4 billion units sold for N8.4 billion, followed by Infracredit Plc with 2.3 billion units traded for N6.5 billion, and Resourcery Plc with 1.1 billion units transacted for N415.7 million.